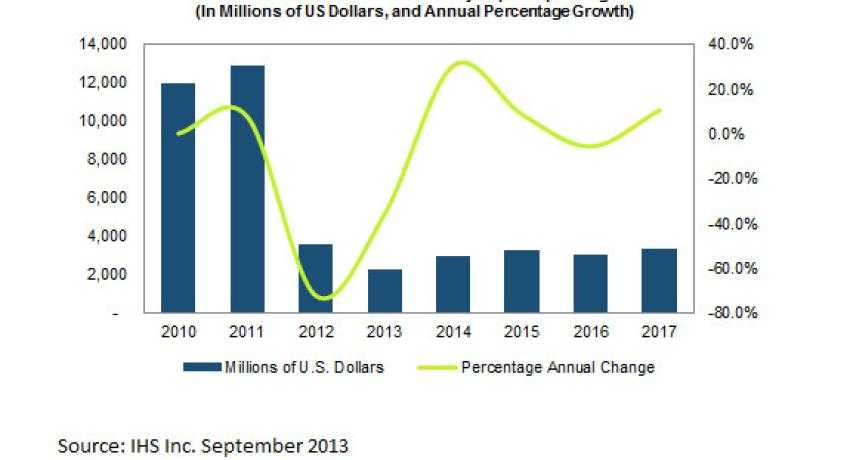

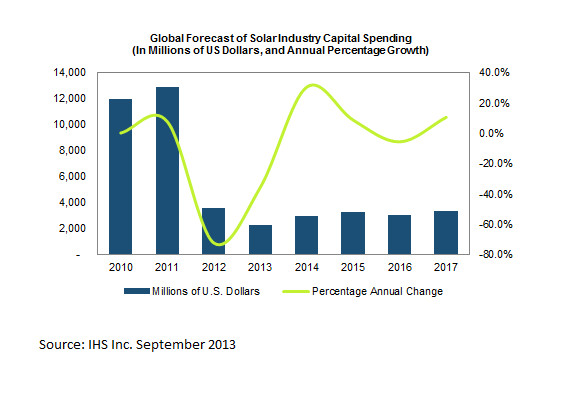

PV Companies Spending Expected to Rise to $3B in 2014

After suffering years of chronic oversupply, it appears that solar companies are now on the rebound, at least according to data from IHS Inc.’s latest PV Manufacturing & Capital Spending Tool. The international analysis company is projecting that PV companies will increase spending on modules, cells, ingots, wafers and polysilicon by up to 30 percent in 2014.

After suffering years of chronic oversupply, it appears that solar companies are now on the rebound, at least according to data from IHS Inc.’s latest PV Manufacturing & Capital Spending Tool. The international analysis company is projecting that PV companies will increase spending on modules, cells, ingots, wafers and polysilicon by up to 30 percent in 2014.

This increase would translate into PV manufacturers spending right around $3 billion and will mark the first time expenditures have risen since 2011, IHS reported. While it's still less than the $3.6 billion manufacturers spent in 2011, it's more than the anticipated $2.3 billion spend that's been projected for 2013.

IHS, however, quickly dismissed the idea that in spending more, the companies may adopt a so-called ‘fabless’ method of manufacturing PV modules.

“Some analysts have claimed that top Chinese and Japanese module makers are utilizing excess manufacturing resources from second- and third-tier manufacturers, expanding their available capacity and thus staving off any requirement for new capital spending,” said Jon Campos, a Solar Analyst at IHS.

“Such a fabless or asset-lite strategy may have worked in other industries, where some companies with minimal or no manufacturing assets—such as Qualcomm Inc. of California—have achieved great success. However, in the PV market, where manufacturing expertise is more proprietary than in other areas, the fabless model is unlikely to be adopted on a large scale,” Campos added. “This means that leading solar suppliers must make capital investments as demand rises in the coming years—even if extra capacity is available from other PV industry suppliers.”

IHS points to recent developments that further show the unlikelihood of fabless production taking place in the solar industry. For example, China made it mandatory that PV manufacturers spend more than 3 percent of their revenue on equipment upgrades, as well as research and development.

“The solar cell business has undergone a transition during the past 24 months,” a spokesperson from IHS stated. “Tier 1 Chinese crystalline suppliers have poured efforts into improving their manufacturing processes.”

Still, company income statements show that at this point, Chinese PV manufacturers are spending more on incremental enhancements in manufacturing than in R&D.

IHS has also observed that the companies are making significant investments of assets and developed significant, in-house expertise.

“Unlike the semiconductor market, this kind of expertise cannot be purchased from equipment providers,” the IHS spokesperson added.

“These companies are very risk averse when it comes to sharing their proprietary process technologies with other manufacturers,” Campos concluded. "They are particularly loath to provide information that could deliver a competitive advantage to companies that have lesser capabilities. The more advanced the modules, the less likely companies are to outsource production to other companies."